New Hampshire Supportive Housing Toolkit

|

Introduction Overview of Permanent Supportive Housing for Persons with Developmental Disabilities Exploration Development Housing Operations Supportive Services Other Living Expenses of Individuals Putting It All Together: Budgeting For The Individual Developing and Maintaining Your Nonprofit Tax-Exempt Entity Additional Resources Glossary |

A) The Development ProcessThe development process includes everything that must happen between the inspiration to create a supported housing setting and moving the first resident into their new home.

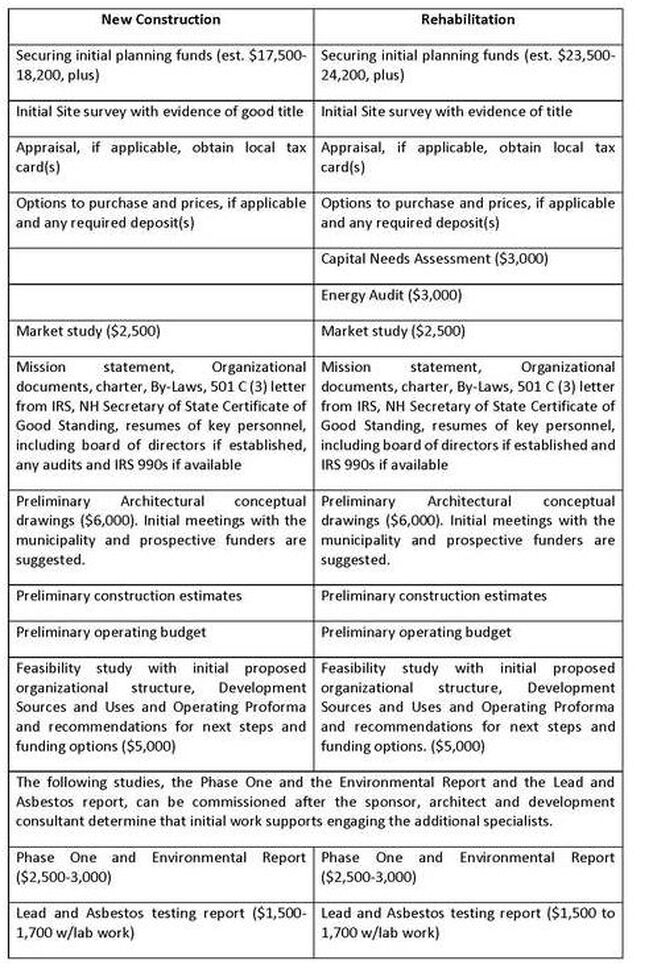

1) The Front EndPre-development, the early stage or front end of the development process, can be expected to take a year or more and cost $25,000 and up for required reports and studies, not including any costs to option or secure property. As discussed above, it’s essential to have a clear vision of the setting one seeks to develop and to be recruiting a team with various skills, knowledge and talents. An architect, civil engineer, development consultant (a person who facilitates the planning for and financing and coordination to ensure that the work plan that was funded is performed) and attorney are important early team members and will often agree to staged or tiered fee arrangements for their work, tied to the various steps of the development process.[1]

View footnotes

[1] For a program with a good reputation and well-defined mission, there may be professionals who will assist at reduced rates. Some professionals will offer free services for worthy and compelling projects. 2) Identifying Potential PropertiesThe development process begins with a clear understanding of the existing need, and what, if anything, is being done now in your area to address that need. Are you the pioneer or have others travelled ahead of you? Who are they and what have they done and learned? What is your vision to address the need in your area? Once articulated, that vision will guide you toward the type physical setting and property needed.

There are a variety of issues which may be relevant to your consideration of a property. Some basic categories include: community acceptance and support; appraisals; zoning; environmental issues; affordability; regional demographics; and access to public transportation. Linked document: Site Selection Criteria and Search Strategies Linked document: Site Analysis 3) Site CharacteristicsSite characteristics matter not only to the sponsor,[1] but also to the sources of funding. Most funders qualify and score applications for grants, deferred and soft loans, and assess project feasibility, based partly on certain of these characteristics.

View footnotes

[1] The sponsor is generally the party that is presenting the initiative in developing a housing project. The sponsor can be the owner, a related party contracted by the owner, a management agent acting on behalf of the owner, or an organization that meets certain standards that the owner cannot (for example where an owner is for-profit). a) Demographic CharacteristicsAre the property’s demographic characteristics considered rural, suburban or urban by the United States Departments of Housing and Urban Development and Agriculture (“USDA”)? A FHLBank of Boston AHP application can receive points if the location qualifies as rural. To determine whether a location qualifies to receive the rural location points, go to USDA’s site http://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do.

Is its census tract considered very-low, low-, moderate- or high-income? To determine whether a FHLBank of Boston AHP application will receive points for economic diversity, the Bank will compare the median family incomes of the census tract in which the project is located (based upon the project address or addresses) to the median family income of the Metropolitan Statistical Area/Metropolitan Division (“MSA/MD”). The median family incomes will be obtained using the Federal Financial Institutions Examination Council’s Geocoding/Mapping and Census Report System, which can be found at www.ffiec.gov. Note that economic diversity can be essential in distinguishing a funding application from those of competing projects. Such diversity can arise either because income in the tract at issue is relatively high (and the project would create diversity by creating affordable units) or because income in the tract at issue is so low that a project’s market units would increase income diversity. b) ZoningWhat zoning restrictions apply to the site? Is the site within a municipal district that will allow the use you plan as a matter of right or prior preference by the community or not? Will you need to work with local officials to enact zoning changes or approve exceptions? Those seeking to develop supportive housing should avoid trying to answer these types of questions on their own. It is essential to engage the town or city planner early in the process to allow them to answer these questions and guide the interested party through the correct steps.

Consider who the neighbors are and what relationships you will need to develop with them. c) AccessibilityDo residents have walking access to local resources and work opportunities or is public transportation available? A title search, identification of any and all easements and a site survey with any existing building locations will be necessary along the way.

Access to public transportation can be essential in distinguishing a funding application from those of competing projects. Where public transportation is not accessible, an AHP application should typically include a representation that the housing operator will bridge the gap to public transportation by providing transportation assistance (for example, as a van to take individuals to and from a bus stop). d) Existing StructuresDoes the site have an existing building? If so, what shape is it in? Does the existing building now house very-low to moderate income people (if so, a relocation plan and budget will be necessary)? How have the building and site been used over the years? Did their use or abutting properties possibly cause environmental impacts? Do the site and building have adequate utilities, soil conditions and drainage for the proposed use? An appraisal will also be needed along the way.

e) Establishing Control of a PropertyOnce a potential property has been identified, the next step is to secure “site control,” meaning some form of right to acquire or lease the property. The type of control that is desirable and possible depends on many factors. It’s crucial to confirm with funders what form(s) of site control will be required or acceptable to meet their requirements.

There are several standard forms of site control:

Any real estate agreement should be prepared by an attorney and, if it binds the buyer, approved by the buyer’s Board of Directors. The buyer should make sure that the closing deadline is far enough away to allow time to complete the necessary acquisition financing. Linked document: Establishing Site Control 5) Predevelopment Site and Structure StudiesOnce you have established some control over the site, a Phase I environmental site assessment will be a necessity. The report is prepared regarding a property to identify existing or potential environmental contamination liabilities. The analysis typically addresses both the underlying land as well as physical improvements to the property and in New Hampshire typically costs $2500 to $3000 per study. An existing building will also require testing for lead and asbestos costing approximately $1500.

Depending on initial results, a Phase II assessment may be required, which is a more detailed investigation involving chemical analysis for hazardous substances and/or petroleum hydrocarbons. If you are going to be rehabbing an existing structure, a Capital Needs Assessment and Energy Audit may be required. If a building was built before 1978, the building and site will need to be tested for the presence of lead and, if built before 1976, tested for asbestos. Older linoleum can contain asbestos, which must be properly removed before demolition. 6) Purchasing PropertyIn structuring a contract of sale or purchase agreement the following should be considered:

The Visions Experience:

|

|

|

View Footnotes

[1] Source: NNEHIF’s 2017 Annual Report.

4) Federal Home Loan Bank of Boston

Federal Home Loan Bank of Boston (“FHLBBoston”) (www.fhlbboston.com). 800 Boylston Street, 9th Floor, Boston, MA 02199, contact Michael Pingpank, Senior Community Investment Manager for New Hampshire, 617-292-9607 or [email protected]. There are twenty-nine New Hampshire member institutions of the FHLBBoston.

Most banks in New England are members. The Federal Home Loan Bank provides capital to members to lend to households, organizations and businesses in their communities. The FHLB makes that capital available to its members at wholesale interest rates. The FHLB also provides certain direct subsidies (grants) and subsidized advances (mortgages at rates at, or below, wholesale rates) for qualified and eligible affordable housing initiatives. See the discussion in the FHLB Section of this Toolkit.

The FHLBank of Boston is the regional Federal Home Loan Bank serving New England. The FHLBank of Boston describes itself, its programs and its membership as follows:

The FHLBank of Boston is one of 11 regional Federal Home Loan Banks established by the Federal Home Loan Bank Act and remains just as vital to the nation's community lenders. Located in Atlanta, Boston, Chicago, Cincinnati, Dallas, Des Moines, Indianapolis, New York, Pittsburgh, San Francisco, and Topeka, the 11 Federal Home Loan Banks help their member financial institutions meet the diverse housing-finance and economic-development needs of their communities.

The Federal Home Loan Bank of Boston is a bank for banks, credit unions, community development financial institutions, and insurance companies. Cooperatively owned by more than 440 New England financial institutions, the Bank provides reliable access to wholesale credit for these members and other qualified borrowers. While New England's borrowers cannot get a loan directly from the FHLBBank, it's very likely that the community bank nearest a potential project is a member that can meet the borrower’s credit needs.

The mission of the Federal Home Loan Bank of Boston is to provide highly reliable wholesale funding, liquidity, and a competitive return on investment to its member financial institutions in New England. The FHLBank of Boston notes that it strives to consistently develop and deliver the best financial products, services, and expertise that support housing finance, community development, and economic growth, including programs targeted to lower-income households.

Through its member institutions, the FHLBank of Boston pursues its mission of facilitation and enhancing of the availability of credit for housing and economic growth, including the housing finance and neighborhood development needs of low- and moderate-income families in communities served by our member institutions. As of October 2018, 29 local banks, credit unions and financial institutions are New Hampshire’s participating owners and members of the FHLBank of Boston, including:

Most banks in New England are members. The Federal Home Loan Bank provides capital to members to lend to households, organizations and businesses in their communities. The FHLB makes that capital available to its members at wholesale interest rates. The FHLB also provides certain direct subsidies (grants) and subsidized advances (mortgages at rates at, or below, wholesale rates) for qualified and eligible affordable housing initiatives. See the discussion in the FHLB Section of this Toolkit.

The FHLBank of Boston is the regional Federal Home Loan Bank serving New England. The FHLBank of Boston describes itself, its programs and its membership as follows:

The FHLBank of Boston is one of 11 regional Federal Home Loan Banks established by the Federal Home Loan Bank Act and remains just as vital to the nation's community lenders. Located in Atlanta, Boston, Chicago, Cincinnati, Dallas, Des Moines, Indianapolis, New York, Pittsburgh, San Francisco, and Topeka, the 11 Federal Home Loan Banks help their member financial institutions meet the diverse housing-finance and economic-development needs of their communities.

The Federal Home Loan Bank of Boston is a bank for banks, credit unions, community development financial institutions, and insurance companies. Cooperatively owned by more than 440 New England financial institutions, the Bank provides reliable access to wholesale credit for these members and other qualified borrowers. While New England's borrowers cannot get a loan directly from the FHLBBank, it's very likely that the community bank nearest a potential project is a member that can meet the borrower’s credit needs.

The mission of the Federal Home Loan Bank of Boston is to provide highly reliable wholesale funding, liquidity, and a competitive return on investment to its member financial institutions in New England. The FHLBank of Boston notes that it strives to consistently develop and deliver the best financial products, services, and expertise that support housing finance, community development, and economic growth, including programs targeted to lower-income households.

Through its member institutions, the FHLBank of Boston pursues its mission of facilitation and enhancing of the availability of credit for housing and economic growth, including the housing finance and neighborhood development needs of low- and moderate-income families in communities served by our member institutions. As of October 2018, 29 local banks, credit unions and financial institutions are New Hampshire’s participating owners and members of the FHLBank of Boston, including:

|

|

Tip: when contacting a local financial institution about working on a project through them with the FHLBBoston, ask to speak with a senior officer or community lending officer who works with the FHLBank of Boston and suggest a conference call with that officer and a staff member of the FHLBank of Boston Housing and Community Investment Department.

The FHLBBoston pursues its mission of facilitation and enhancing the availability of credit for housing and economic growth, including the housing finance and neighborhood development needs of low- and moderate-income families in communities served by our member institutions. To accomplish its mission, the Bank prudently and effectively utilizes private-sector capital to provide members and other qualified customers with reliable access to low-cost wholesale funds, liquidity, and competitive outlet for the sale of loans, special lending programs, education and technical assistance, and other products and services. The Bank offers its members the following options for funding affordable housing and economic development:

The FHLBBoston pursues its mission of facilitation and enhancing the availability of credit for housing and economic growth, including the housing finance and neighborhood development needs of low- and moderate-income families in communities served by our member institutions. To accomplish its mission, the Bank prudently and effectively utilizes private-sector capital to provide members and other qualified customers with reliable access to low-cost wholesale funds, liquidity, and competitive outlet for the sale of loans, special lending programs, education and technical assistance, and other products and services. The Bank offers its members the following options for funding affordable housing and economic development:

a) The Affordable Housing Program

The Affordable Housing Program (“AHP”) supports the Federal Home Loan Bank of Boston's efforts to address, in partnership with member institutions, the affordable-housing needs of communities across New England. A portion of the Bank's earnings funds the program, which awards grant and low-interest advances, or loans, through member institutions. The program provides financing for homeownership and rental housing for households with incomes at or below 80 percent of the median income for the area. Maximum direct subsidy awards or grants with 15-year obligations to maintain project characteristics are $500,000 per project with a total AHP subsidy award of $1,000,000 possible, the second $500,000 being in the form of a rate reduction on a long term fixed rate (up to a 30-year term) known as a “subsidized advance” or mortgage from the FHLBBoston to the member bank passed through the member to the project sponsor. (Note: any such advance, if prepaid, could experience a prepayment fee assessment.)

The Affordable Housing Program allows the Federal Home Loan Bank of Boston to address, in partnership with member institutions, affordable-housing needs primarily in communities across New England. A portion of the Bank's net earnings (10% annually) funds the program, which awards grants and low-interest advances, or loans, through member institutions. The AHP encourages local planning of affordable-housing initiatives. The Bank's member institutions work with local housing organizations to apply for funds to support initiatives that serve very low- to moderate-income households in their communities. Each year, funding for projects submitted to the AHP by member institutions is awarded in at least one competitive round. Subsidized loans (advances) and direct subsidies (grants) are available. The actual terms are determined by the member financial-institution applicant, based on the specific needs of the development.

Both homeownership and rental initiatives can qualify for Affordable Housing Program (AHP) funding, so long as they meet certain criteria. Wherever mentioned in this AHP information, area median income means the area median income as defined by the U.S. Department of Housing and Urban Development (HUD). Consult HUD's Web site for the latest median income guidelines. HUD Multifamily Tax Subsidy Limits (MTS) are utilized with initiatives using Low Income Housing Tax Credits, the income limits used for 50 and 60 percent of the area median income will be the HUD Multifamily Tax Subsidy Project limits as adjusted for household size.

AHP funding can be used to finance homeownership initiatives for households with incomes at or below 80 percent of the median income for the area. Examples of eligible uses include single-family houses, subdivisions, cooperatives, condominiums, down-payment and closing-cost assistance, and mobile-home parks.

AHP funding may also be used to finance rental housing in which at least 20 percent of the units are for households with incomes that do not exceed 50 percent of the median income for the area. Examples of eligible uses include multifamily rental housing, single-room-occupancy (SRO) housing, and mutual housing.

Program funds may be used only for the direct costs of producing or financing affordable housing. Uses include acquisition, construction, rehabilitation costs, related soft costs, interest-rate buy-downs, down-payment and closing-cost assistance, and matched-savings programs. Only those units that are affordable, as defined by AHP regulations, are eligible for funding. Supportive services and commercial space associated with a development are ineligible for AHP funding.

The development sponsor must pass the benefits of the AHP funding through to the initiative and/or end user. The developer/sponsor cannot retain any portion of the AHP funds as profit or for the purpose of additional development (excluding approved development fees). AHP funds may not be "recycled," or used for capitalized operating reserves or for nonresidential space.

The scoring criteria for the Affordable Housing Program are as follows:

The Affordable Housing Program allows the Federal Home Loan Bank of Boston to address, in partnership with member institutions, affordable-housing needs primarily in communities across New England. A portion of the Bank's net earnings (10% annually) funds the program, which awards grants and low-interest advances, or loans, through member institutions. The AHP encourages local planning of affordable-housing initiatives. The Bank's member institutions work with local housing organizations to apply for funds to support initiatives that serve very low- to moderate-income households in their communities. Each year, funding for projects submitted to the AHP by member institutions is awarded in at least one competitive round. Subsidized loans (advances) and direct subsidies (grants) are available. The actual terms are determined by the member financial-institution applicant, based on the specific needs of the development.

Both homeownership and rental initiatives can qualify for Affordable Housing Program (AHP) funding, so long as they meet certain criteria. Wherever mentioned in this AHP information, area median income means the area median income as defined by the U.S. Department of Housing and Urban Development (HUD). Consult HUD's Web site for the latest median income guidelines. HUD Multifamily Tax Subsidy Limits (MTS) are utilized with initiatives using Low Income Housing Tax Credits, the income limits used for 50 and 60 percent of the area median income will be the HUD Multifamily Tax Subsidy Project limits as adjusted for household size.

AHP funding can be used to finance homeownership initiatives for households with incomes at or below 80 percent of the median income for the area. Examples of eligible uses include single-family houses, subdivisions, cooperatives, condominiums, down-payment and closing-cost assistance, and mobile-home parks.

AHP funding may also be used to finance rental housing in which at least 20 percent of the units are for households with incomes that do not exceed 50 percent of the median income for the area. Examples of eligible uses include multifamily rental housing, single-room-occupancy (SRO) housing, and mutual housing.

Program funds may be used only for the direct costs of producing or financing affordable housing. Uses include acquisition, construction, rehabilitation costs, related soft costs, interest-rate buy-downs, down-payment and closing-cost assistance, and matched-savings programs. Only those units that are affordable, as defined by AHP regulations, are eligible for funding. Supportive services and commercial space associated with a development are ineligible for AHP funding.

The development sponsor must pass the benefits of the AHP funding through to the initiative and/or end user. The developer/sponsor cannot retain any portion of the AHP funds as profit or for the purpose of additional development (excluding approved development fees). AHP funds may not be "recycled," or used for capitalized operating reserves or for nonresidential space.

The scoring criteria for the Affordable Housing Program are as follows:

|

A. Initiatives that finance the purchase, construction, and/or rehabilitation of owner-occupied housing for very low-, low-, and moderate-income households (any household for which the aggregate income is 80 percent or less of the area median income as determined and published by the United States Department of Housing and Urban Development) for the retention period of five years; or

B. Initiatives that finance the purchase, construction, and/or rehabilitation of rental housing, of which at least 20 percent of the units will be occupied by and affordable for very low-income households (50 percent or less of the area median income as determined and published by the United States Department of Housing and Urban Development) for the retention period of 15 years. |

Points are awarded as follows:

Each year, the Federal Home Loan Bank of Boston, in consultation with its Advisory Council, develops an implementation plan for its Affordable Housing Program. See the Affordable Housing Program Implementation Plan by clicking on the website at http://www.fhlbboston.com/communitydevelopment/ahp/03_01_06_implementation.jsp. Applications are submitted once a year usually in late July[1] on line after meeting with the local members bank to secure their participation and registering on the website with the Community and Housing Investment Department for that round of the AHP.

Once completed, initiatives funded through the Affordable Housing Program are subject to the following reporting requirements. All reports are available online.

Reporting: Semiannual Progress Reports are required until the project is complete. Upon completion of an initiative, Bank staff compare the completed project with that which was proposed in the application to determine whether the project remains in compliance with the AHP regulation. Members and project sponsors must submit an Annual Compliance Certification annually for 15 years for rental developments. Members and project sponsors/owners that have a rental development receiving more than $50,000 in AHP subsidy must submit a Periodic Monitoring Report once every six years. Projects receiving more than $250,000 must submit a Periodic Monitoring Report once every four years and rental developments receiving equal to or greater than $500,000 must submit a Periodic Monitoring Report once every two years. Please note: For initiatives requiring this report, the Period Monitoring Report has been combined with the Annual Compliance Certification (ACCPMR).

Changes, noncompliance and recapture. Sponsors and members have the obligation for the first 15-years to report any changes, or events of noncompliance, to the FHLBBoston. FHLBBoston has a Watch List system, a Workout process and a Procedure for recapturing any AHP funds in AHP-funded initiatives in which the project sponsor has failed to meet its contractual mortgages under the FHBBoston’s agreements, mortgage and documents.

2018 New Hampshire AHP awards: In December 2018 four New Hampshire affordable housing projects with a total of 133 units were awarded a combined $6.7 million in grants and loans in the Federal Home Loan Bank of Boston’s 2018 AHP round.

The support, awarded to four New Hampshire banks through the FHLB’s Affordable Housing Program, is part of $46.6 million in funding given to 47 projects with 2,550 units around New England.

The grants and loans will be used to help pay construction, acquisition and rehabilitation costs. Member banks work with local developers to apply for funding, which is awarded through a competitive scoring process.

Awarded funding in New Hampshire were:

- Targeting consistent with the ownership or rental priorities described above (up to 20 points with 60% of the units targeted for residents earning at or below 50% AMI)

- Use of donated federal-government-owned or other properties (up to 5 points)

- Sponsorship by a not-for-profit organization or government entity (up to 5 points)

- Housing for homeless households (up to 5 points)

- Promotion of empowerment (up to 10 points)

- First-time home buyers (up to 5 points)

- Financial participation by the member (up to 12.5 points)

- Economic diversity (5 points)

- Community stability (up to 15 points)

- Effectiveness — AHP subsidy per unit (up to 5 points)

- Initiatives located in rural areas (5 points)

- Second District Priority (7.5 points)

Each year, the Federal Home Loan Bank of Boston, in consultation with its Advisory Council, develops an implementation plan for its Affordable Housing Program. See the Affordable Housing Program Implementation Plan by clicking on the website at http://www.fhlbboston.com/communitydevelopment/ahp/03_01_06_implementation.jsp. Applications are submitted once a year usually in late July[1] on line after meeting with the local members bank to secure their participation and registering on the website with the Community and Housing Investment Department for that round of the AHP.

Once completed, initiatives funded through the Affordable Housing Program are subject to the following reporting requirements. All reports are available online.

Reporting: Semiannual Progress Reports are required until the project is complete. Upon completion of an initiative, Bank staff compare the completed project with that which was proposed in the application to determine whether the project remains in compliance with the AHP regulation. Members and project sponsors must submit an Annual Compliance Certification annually for 15 years for rental developments. Members and project sponsors/owners that have a rental development receiving more than $50,000 in AHP subsidy must submit a Periodic Monitoring Report once every six years. Projects receiving more than $250,000 must submit a Periodic Monitoring Report once every four years and rental developments receiving equal to or greater than $500,000 must submit a Periodic Monitoring Report once every two years. Please note: For initiatives requiring this report, the Period Monitoring Report has been combined with the Annual Compliance Certification (ACCPMR).

Changes, noncompliance and recapture. Sponsors and members have the obligation for the first 15-years to report any changes, or events of noncompliance, to the FHLBBoston. FHLBBoston has a Watch List system, a Workout process and a Procedure for recapturing any AHP funds in AHP-funded initiatives in which the project sponsor has failed to meet its contractual mortgages under the FHBBoston’s agreements, mortgage and documents.

2018 New Hampshire AHP awards: In December 2018 four New Hampshire affordable housing projects with a total of 133 units were awarded a combined $6.7 million in grants and loans in the Federal Home Loan Bank of Boston’s 2018 AHP round.

The support, awarded to four New Hampshire banks through the FHLB’s Affordable Housing Program, is part of $46.6 million in funding given to 47 projects with 2,550 units around New England.

The grants and loans will be used to help pay construction, acquisition and rehabilitation costs. Member banks work with local developers to apply for funding, which is awarded through a competitive scoring process.

Awarded funding in New Hampshire were:

- Franklin Savings Bank, $350,000 in support of improvements at Lakes Region Community Developers’ Harvey Heights Phase I project in Ashland, affecting 40 rental units. Proposed improvements include installation of a sprinkler system, upgrading the fire alarm system, window and siding replacement, improved insulation, addition of water-conserving bathroom fixtures and roofing replacement.

- Bangor Savings Bank, $439,200 in support of Avesta Housing Development Corp.’s project to rehabilitate and refinance 11 units at a rent-subsidized property in Farmington. Corporation co-sponsor is Saco Housing Development.

- Ledyard National Bank, a $729,944 grant and subsidy and a $601,000 loan in support of Twin Pines Housing Trust’s Summer Park Residences Phase 2, which will include 18 rental units for seniors and individuals with disabilities.

- The Provident Bank, a $999,657 grant and subsidy and $3,650,000 loan in support of the Portsmouth Housing Authority’s Court Street workforce housing project in Portsmouth. The project involves construction of a four-story building with a subsurface parking garage to create 64 low-income rental apartments.

View Footnotes

[1] As of 2019.

b) The Equity Builder Program

The Equity Builder Program (EBP) offers members grants to provide households with incomes less than 80 percent of the area median income with down-payment, closing-cost, home-buyer counseling, and rehabilitation assistance. Members can also use EBP grants to match eligible buyers' savings. The EBP is funded by a percentage of the Bank's annual AHP subsidy.

c) Community Development Advance Program

Whether a community needs capital for small business, fixed-rate financing for affordable housing, or improvements to local roads or schools, members can turn to the Federal Home Loan Bank of Boston's Community Development Advance Program. These advances, which are subject to specific income limits, are available through two separate application options that help support community development activities: CDA Extra and CDA.

d) New England Fund

The New England Fund (NEF) provides member financial institutions with advances to support housing and community-development initiatives that benefit moderate-income households and neighborhoods. The NEF serves a broader range of moderate-income households than the Bank's Community Development Advance and provides special flexibility for mixed-income residential development.

e) Jobs for New England

The Jobs for New England program (“JNE”) is a three-year, $15 million subsidy program dedicated to supporting job growth and economic development throughout New England. The subsidy will be used to write down interest rates to zero percent on Classic advances that finance qualifying loans to small businesses. Beginning February 1, 2016, JNE provided up to $5 million per year through 2018 on a first-come, first-served basis, with a maximum of $250,000 of interest subsidy available per member per year; JNE advances will not be subject to any prepayment fees. JNE has been reauthorized. The FHLBBoston recently (winter, 2019) extended the program.

f) Helping to House New England

The Helping to House New England program (HHNE) is a three-year, $15 million interest-rate subsidy program dedicated to expanding affordable rental and homeownership financing through the six New England Housing Finance Agencies. Beginning February 1, 2016, HHNE provided up to $5 million per year through 2018 on an estimated per-capita basis to each of the New England HFAs. NHHFA has made use of this program. The subsidy was used to write down interest rates to zero percent on Classic advances for the purpose of expanding affordable rental and homeownership initiatives. HHNE has been reauthorized for an additional three years. The FHLBBoston recently (winter, 2019) extended the program.

5) Thinking Creatively About Potential Sources of Housing Capital

a) Fund-Raising Activities In Sponsors’ Respective Geographic Area(s) And In Their Communities Of Interest

An entity with an interest in developing affordable housing should consider preparing a five-year rolling plan to focus part of the entity’s attention on educating boards of directors and interested parties and supporters about area need and opportunities. One way of accomplishing this part of a plan is to identify or create a signature annual event that engages, educates, and involves the wider community.

Some organizations host a road race or a golf outing, others create a food event, undertake building a house, restoring a park, conducting a community-wide work day to help seniors, holding a barn raising or sponsoring a music or film festival. While funds raised may not always be impactful, the community engagement and the education can be enduring. Such events encourage investment in the sponsor’s mission by the wider community. Moreover, it is an annual opportunity to provide recognition to, and express appreciation for, board members, funders, vendors, suppliers, tradespeople and community leaders and volunteers who provide the foundation for the organization’s accomplishments every year.

Some organizations host a road race or a golf outing, others create a food event, undertake building a house, restoring a park, conducting a community-wide work day to help seniors, holding a barn raising or sponsoring a music or film festival. While funds raised may not always be impactful, the community engagement and the education can be enduring. Such events encourage investment in the sponsor’s mission by the wider community. Moreover, it is an annual opportunity to provide recognition to, and express appreciation for, board members, funders, vendors, suppliers, tradespeople and community leaders and volunteers who provide the foundation for the organization’s accomplishments every year.

b) Seller Financing

In seller financing, rather than a buyer taking a loan from a bank, the person selling the property lends the buyer the money for the purchase. Buyer and seller execute a promissory note providing an interest rate, repayment schedule, and for the consequences of default. The buyer makes her monthly mortgage payments to the seller, who earns interest on the loan at a rate which may vary considerably from marketplace rates.

The Visions Experience: Seller Financing

The land and structures which were to become Vision’s campus at Sunrise Farm were already owned by the founding Dow family. The Dows transferred title to Visions in a seller financing transaction, permitting Visions to avoid many of the challenges presented by having to raise capital funding. The Dows became the mortgagees and Visions became the mortgagor, making monthly payments of principal and interest to the Dows at a deeply-discounted fixed rate. This benefitted Visions in several ways unique to the circumstances and unlikely to be duplicated in other situations. First, the existing structures (a former inn and out buildings) lent themselves to conversion to Visions with (at least at the outset) minimal rehab. Second, the Dows had both the personal experience with the property and the expertise which permitted them to make the property operable without costly investment in rehab. Third, the Dows supported the enterprise by valuing the property for purposes of seller financing at the town’s assessed value – potentially considerably under market. Fourth, the Dows’ deeply discounted long-term mortgage provided a rate and term seldom available in multi-family borrowing.

One point to bear in mind with respect to seller financing or any kind of borrowing: consider the long term consequences. While Visions was fortunate to be able to acquire Sunrise Farm at the advantageous rate and term that the Dows offered, as refinancing becomes necessary in the future, increased costs may apply.

The lesson is that sponsors and owners should think carefully (and seek expert advice) about how they want to fund their project early on, get the help they need to conceptualize it for the long haul early on and determine their best options.

A supportive housing project starting out would need to identify ways to replace the unique value Visions enjoyed. There ought to be some value in hand, from fund raising from families and other sources, before seeking bank funding for property, construction or rehab.

One point to bear in mind with respect to seller financing or any kind of borrowing: consider the long term consequences. While Visions was fortunate to be able to acquire Sunrise Farm at the advantageous rate and term that the Dows offered, as refinancing becomes necessary in the future, increased costs may apply.

The lesson is that sponsors and owners should think carefully (and seek expert advice) about how they want to fund their project early on, get the help they need to conceptualize it for the long haul early on and determine their best options.

A supportive housing project starting out would need to identify ways to replace the unique value Visions enjoyed. There ought to be some value in hand, from fund raising from families and other sources, before seeking bank funding for property, construction or rehab.

c) Strategies to Make LIHTCs More Relevant to Supportive Housing

Despite the fact that LIHTCs are the preeminent source of affordable housing funding, there are issues which limit the likelihood that a supportive housing project will find LIHTCs to be a good fit. Relying on LIHTCs imposes years of on-going administrative diligence (determining and documenting resident income eligibility) and related federal reporting requirements, obligations which are more burdensome and costly per unit to the extent the cost of that administrative burden is spread across fewer units. The need to increase the number of units in a contemplated development, in order to make using LIHTCs feasible, conflicts with the need to limit the number of units to ensure the setting will be one in which Medicaid services are permitted to be delivered under the Settings Rule.

NHHFA has been recommending that projects be at least twenty units to make LIHTC funding feasible. However that is not a hard and fast rule, and state affordable housing agencies around the U.S. have been experimenting with funding increasingly smaller developments through LIHTCs. Because of these changing assumptions, if you are contemplating developing housing, reach out to your state affordable housing agency or to an experienced consultant for more current information.

One possible way to address the size conflict would be to explore whether a project involving multiple sites could qualify as an applicant for tax credits. Another possible way to resolve the conflict would be to partner with an affordable housing developer in developing a setting in which only a minority of the units are earmarked to provide supportive housing in which Medicaid services will be delivered. Any such an exploratory conversation with a developer should take place as early as possible in the process.

As of this writing, a number of projects around the U.S. are pursuing strategies in this area.

One Wisconsin supported housing project, in the pre-development phase as of this writing, aims to create supported housing within a larger affordable housing development.[1] The forty-unit rural project, Home Of Our Own,[2] would have ten units of supportive housing for adults with developmental disabilities, the balance of the units income-based affordable housing. The founding families with adult children with I/DD brought in a local affordable housing developer to partner, secured an option on a six-acre parcel, retained architects, and have applied for the tax credit funding. (A decision on the LIHTC application was due in March, 2019; they hope to open for residents by the fall of 2020.) The developer committed $500,000; the families are trying to fundraise another $500,000 toward the project’s $8 million capital budget. The forward-looking project, designed to include communal spaces, gardens and walking paths, aims to serve persons with disabilities across the spectrum of independence and low-income tenants from young workers to retirees.

A project in Rockville, Maryland, although it will not provide supports,[3] aims to serve persons with developmental disabilities in an integrated setting.[4] Main Street[5] is a seven-story, 70-unit apartment building anticipated to open in 2020 where three quarters of the units will be affordable housing, a third of the affordable units being designed and designated for adults with special needs. The balance of the apartments will rent at market rate. The $30 million nonprofit organization will receive tax credits, along with private and public funding. Planned as an inclusive, community-centered residential development, the developers (a family[6] with a special needs adult child) seek to create a model in offering not only an inclusive community for residents with social engagement, accessibility and educational, vocational and therapeutic programming, but also fostering community integration by making programming available to non-residents on a subscription membership model. The complex will consist of one-, two- and three-bedroom apartments, along with a cafe, a movie room, an art gallery, a teaching kitchen and a yoga and wellness center. The space is designed to encourage formal and informal hanging out. The half-acre plot, across the street from a public transportation rail station, was sold to the family by a friend. Although the complex is not yet signing up residents, more than 1,300 people have become members.

In Virginia, the Faison Center[7] (focused on persons with autism) operates a residence featuring forty-five apartments, as well as a community room and recreational facilities for social activities. Approximately a third of the apartments are set aside for adult tenants with autism and other developmental disabilities who are generally independent but need occasional assistance and supervision. The remaining apartments are rented to the public. The residence allows individuals to live as independently as possible with supportive in-home services.

There are also examples of supportive housing developed for persons with developmental disabilities and economic means. One is First Place–Phoenix,[8] located in downtown Phoenix, Arizona. The 55-unit apartment property is designed to be community connected, transit-oriented and sustained by a suite of supports and amenities, serving residents with autism and other special needs.

To track developments in this area, HUD maintains an inventory of tax credit housing at www.huduser.org/DATASETS/lihtc.html.

There are parallel developments around the world. See for example in Australia the Youngcare effort. (https://www.youngcare.com.au/what-we-do/housing/).

NHHFA has been recommending that projects be at least twenty units to make LIHTC funding feasible. However that is not a hard and fast rule, and state affordable housing agencies around the U.S. have been experimenting with funding increasingly smaller developments through LIHTCs. Because of these changing assumptions, if you are contemplating developing housing, reach out to your state affordable housing agency or to an experienced consultant for more current information.

One possible way to address the size conflict would be to explore whether a project involving multiple sites could qualify as an applicant for tax credits. Another possible way to resolve the conflict would be to partner with an affordable housing developer in developing a setting in which only a minority of the units are earmarked to provide supportive housing in which Medicaid services will be delivered. Any such an exploratory conversation with a developer should take place as early as possible in the process.

As of this writing, a number of projects around the U.S. are pursuing strategies in this area.

One Wisconsin supported housing project, in the pre-development phase as of this writing, aims to create supported housing within a larger affordable housing development.[1] The forty-unit rural project, Home Of Our Own,[2] would have ten units of supportive housing for adults with developmental disabilities, the balance of the units income-based affordable housing. The founding families with adult children with I/DD brought in a local affordable housing developer to partner, secured an option on a six-acre parcel, retained architects, and have applied for the tax credit funding. (A decision on the LIHTC application was due in March, 2019; they hope to open for residents by the fall of 2020.) The developer committed $500,000; the families are trying to fundraise another $500,000 toward the project’s $8 million capital budget. The forward-looking project, designed to include communal spaces, gardens and walking paths, aims to serve persons with disabilities across the spectrum of independence and low-income tenants from young workers to retirees.

A project in Rockville, Maryland, although it will not provide supports,[3] aims to serve persons with developmental disabilities in an integrated setting.[4] Main Street[5] is a seven-story, 70-unit apartment building anticipated to open in 2020 where three quarters of the units will be affordable housing, a third of the affordable units being designed and designated for adults with special needs. The balance of the apartments will rent at market rate. The $30 million nonprofit organization will receive tax credits, along with private and public funding. Planned as an inclusive, community-centered residential development, the developers (a family[6] with a special needs adult child) seek to create a model in offering not only an inclusive community for residents with social engagement, accessibility and educational, vocational and therapeutic programming, but also fostering community integration by making programming available to non-residents on a subscription membership model. The complex will consist of one-, two- and three-bedroom apartments, along with a cafe, a movie room, an art gallery, a teaching kitchen and a yoga and wellness center. The space is designed to encourage formal and informal hanging out. The half-acre plot, across the street from a public transportation rail station, was sold to the family by a friend. Although the complex is not yet signing up residents, more than 1,300 people have become members.

In Virginia, the Faison Center[7] (focused on persons with autism) operates a residence featuring forty-five apartments, as well as a community room and recreational facilities for social activities. Approximately a third of the apartments are set aside for adult tenants with autism and other developmental disabilities who are generally independent but need occasional assistance and supervision. The remaining apartments are rented to the public. The residence allows individuals to live as independently as possible with supportive in-home services.

There are also examples of supportive housing developed for persons with developmental disabilities and economic means. One is First Place–Phoenix,[8] located in downtown Phoenix, Arizona. The 55-unit apartment property is designed to be community connected, transit-oriented and sustained by a suite of supports and amenities, serving residents with autism and other special needs.

To track developments in this area, HUD maintains an inventory of tax credit housing at www.huduser.org/DATASETS/lihtc.html.

There are parallel developments around the world. See for example in Australia the Youngcare effort. (https://www.youngcare.com.au/what-we-do/housing/).

View Footnotes

[1] See news coverage at https://www.washingtonpost.com/lifestyle/2019/01/29/faced-with-few-options-these-moms-are-building-home-their-adult-autistic-children/?utm_term=.d8c91513d32f&noredirect=on. See also https://www.wpr.org/wisconsin-parents-team-build-housing-their-adult-children-disabilities.

[2] https://www.facebook.com/HOOOWisconsin/

[3] Rather than supportive living, Main Street will offer independent housing. Persons who need supports will bring their own, as they would when renting any apartment. As all renters will have their own choice, key and decorate their own rented apartment, the Maryland Developmental Disabilities Administration does not consider Main Street to represent congregate care and has supported the development with a two million dollar capital grant.

[4] See news coverage at https://www.washingtonpost.com/local/social-issues/rockville-parents-build-a-home-for-their-developmentally-disabled-kids/2019/02/12/d34e6c9a-2be3-11e9-b011-d8500644dc98_story.html?noredirect=on.

[5] https://mainstreetconnect.org/

[6] A member of the family is a professional developer, who reportedly waived his fees, as did the interior designers.

[7] https://www.faisoncenter.org/the-faison-residence

[8] https://www.firstplaceaz.org/

[2] https://www.facebook.com/HOOOWisconsin/

[3] Rather than supportive living, Main Street will offer independent housing. Persons who need supports will bring their own, as they would when renting any apartment. As all renters will have their own choice, key and decorate their own rented apartment, the Maryland Developmental Disabilities Administration does not consider Main Street to represent congregate care and has supported the development with a two million dollar capital grant.

[4] See news coverage at https://www.washingtonpost.com/local/social-issues/rockville-parents-build-a-home-for-their-developmentally-disabled-kids/2019/02/12/d34e6c9a-2be3-11e9-b011-d8500644dc98_story.html?noredirect=on.

[5] https://mainstreetconnect.org/

[6] A member of the family is a professional developer, who reportedly waived his fees, as did the interior designers.

[7] https://www.faisoncenter.org/the-faison-residence

[8] https://www.firstplaceaz.org/

d) Project-Based § 8 & § 811 Housing Subsidies

The project-based HUD-funded programs give owners the option of dedicating facilities to elderly residents, residents with disabilities, or both populations together.

Proposals for Project-Based Vouchers (“PBV”s) are selected by NHFFA by one of the following two methods.

Housing Choice Voucher Administrative Plan 2018, p. 76.

At present in New Hampshire, Section 811 subsidies[1] are limited to projects serving persons with mental illness, but that might change over time.

Proposals for Project-Based Vouchers (“PBV”s) are selected by NHFFA by one of the following two methods.

- NHHFA may solicit proposals by using a request for proposals to select proposals on a competitive basis. NHHFA will not limit proposals to a single site or impose restrictions that explicitly or practically preclude owner submission of proposals for PBV housing on different sites.

- NHHFA may select proposals for housing assisted under a federal, state, or local government housing assistance, community development, or supportive services program that requires competitive selection of proposals (e.g., HOME, and units for which competitively awarded LIHTC’s have been provided), where the proposal has been selected in accordance with such program's competitive selection requirements within three years of the PBV proposal selection date, and the earlier competitive selection proposal did not involve any consideration that the project would receive PBV assistance.

Housing Choice Voucher Administrative Plan 2018, p. 76.

At present in New Hampshire, Section 811 subsidies[1] are limited to projects serving persons with mental illness, but that might change over time.

View Footnotes

1] The Housing and Urban Development Supportive Housing for Persons with Disabilities Section 811 PRA Program (“§ 811”) provides affordable and accessible housing for adults with disabilities 18 or older, but less than 62, and their family. The § 811 program is authorized to provide capital grants and project rental assistance to nonprofit developers of housing targeted specifically to persons with disabilities. The program is operated by New Hampshire Housing Finance Authority in partnership with the New Hampshire Department of Health and Human Services, Division for Behavioral Health, Bureau of Mental Health Services.

Prior to creation of Section 811, persons with disabilities lived together with elderly residents (defined by HUD as households with one or more adults age 62 or older) in developments funded through the Section 202 Supportive Housing for the Elderly program.

Tenants who qualify for this program pay no more than 30% of their adjusted income for rent and utilities while continuing to have access to support services. The 811 Program is not a tenant-based program where the tenant retains the housing assistance when they move; the housing subsidy is connected to the property. Federal FY19 budgeting provided funding to renew existing contracts for Section 811 Housing for Persons with Disabilities.

Prior to creation of Section 811, persons with disabilities lived together with elderly residents (defined by HUD as households with one or more adults age 62 or older) in developments funded through the Section 202 Supportive Housing for the Elderly program.

Tenants who qualify for this program pay no more than 30% of their adjusted income for rent and utilities while continuing to have access to support services. The 811 Program is not a tenant-based program where the tenant retains the housing assistance when they move; the housing subsidy is connected to the property. Federal FY19 budgeting provided funding to renew existing contracts for Section 811 Housing for Persons with Disabilities.

Linked document: Section 811 Fact Sheet

Contact NHHFA for information concerning current project-based § 8 and § 811 programs.

e) Equity Investors

At some price point, equity investment in supported housing, built with a sufficient proportion of upfront public affordable housing funding and enjoying ongoing income streams through SSI and Section 8, and perhaps additional favorable tax treatment, will offer sufficient promise of return to bring private money into supportive housing development.

While investors’ appetites for diversification and hedging (and financial returns) continue to create vibrant markets for real estate investing, there is not yet a robust market seeking investment in supportive housing as a sector. Equity investment interest in the broader category of affordable housing, on the other hand, continues to develop, often under the banner of “impact investing,” sometimes managed by mission-oriented entities. Seeking to heighten interest among investors in supportive housing will presumably involve one part consciousness-raising and one part pitching the advantages supportive housing may present to developers and investors in affordable housing. More on those below.

When it comes to supportive housing, a likely necessary precondition for investment opportunities to arise is the separation of the building and operation of the physical plant from the costly and perennially under-funded supports and services component. Some creativity might be required.[1] Note that while a for-profit business could subsidize an affordable housing entity, affordable housing could not be seen as subsidizing a for-profit business.[2]

The economics of operating Supportive Housing, standing alone, do not appear to be able to provide a rate of return which would attract equity investors.[3] As appears to be the case with utilizing LIHTCs, developing supportive housing units as part of a larger, mixed-use affordable housing project may be the only context in which equity investment might be relevant, at present.[4] In addition to bearing equity in mind as a potential funding source in developing mixed use affordable housing, there are several long-term trends which could lead to the availability of equity investing for stand-alone supportive housing in the future.

First, a growing percentage of investors seek positive social impact along with their financial returns.[5] Most such investors seek market-rate returns in addition to social impact, so growth in this trend, alone, may not be sufficient to bring equity investors into the field. Creative new manifestations are bubbling up in this sector daily. In addition to traditional equity, there are unexpected players: for example, the New York arm of Habitat for Humanity recently announced plans to establish a community development financial institution to lend investors’ money to housing projects in the city. Its set-up costs have been financed by Deutsche Bank.[6]

Second, contemporary investors have sought diversification in increasingly arcane slices of the greater market for real estate, creating the possibility that attributes of the financing of supportive housing development might find a match with a class of investors.

While investors’ appetites for diversification and hedging (and financial returns) continue to create vibrant markets for real estate investing, there is not yet a robust market seeking investment in supportive housing as a sector. Equity investment interest in the broader category of affordable housing, on the other hand, continues to develop, often under the banner of “impact investing,” sometimes managed by mission-oriented entities. Seeking to heighten interest among investors in supportive housing will presumably involve one part consciousness-raising and one part pitching the advantages supportive housing may present to developers and investors in affordable housing. More on those below.

When it comes to supportive housing, a likely necessary precondition for investment opportunities to arise is the separation of the building and operation of the physical plant from the costly and perennially under-funded supports and services component. Some creativity might be required.[1] Note that while a for-profit business could subsidize an affordable housing entity, affordable housing could not be seen as subsidizing a for-profit business.[2]

The economics of operating Supportive Housing, standing alone, do not appear to be able to provide a rate of return which would attract equity investors.[3] As appears to be the case with utilizing LIHTCs, developing supportive housing units as part of a larger, mixed-use affordable housing project may be the only context in which equity investment might be relevant, at present.[4] In addition to bearing equity in mind as a potential funding source in developing mixed use affordable housing, there are several long-term trends which could lead to the availability of equity investing for stand-alone supportive housing in the future.

First, a growing percentage of investors seek positive social impact along with their financial returns.[5] Most such investors seek market-rate returns in addition to social impact, so growth in this trend, alone, may not be sufficient to bring equity investors into the field. Creative new manifestations are bubbling up in this sector daily. In addition to traditional equity, there are unexpected players: for example, the New York arm of Habitat for Humanity recently announced plans to establish a community development financial institution to lend investors’ money to housing projects in the city. Its set-up costs have been financed by Deutsche Bank.[6]

Second, contemporary investors have sought diversification in increasingly arcane slices of the greater market for real estate, creating the possibility that attributes of the financing of supportive housing development might find a match with a class of investors.

View Footnotes

[1] For example Sunrise Farm has common rooms in the residential setting which could be used by an organization providing services to the residents. That should be a legitimate use of the space, from the view of affordable housing funders. But, especially if persons other than the residents were to be served, it might make sense to condo out the office space. Or the organization providing service to the residents could pay rent to the owner of the physical plant.

[2] While it is beyond the scope of this Toolkit, a tax credit program exists for developing businesses, something of a corollary to the LIHTC program for residential development: the New Markets Tax Credit Program. See www.cdfifund.gov/Documents/NMTC%20Target%20Areas%20QA.pdf and www.taxpolicycenter.org/briefing-book/what-new-markets-tax-credit-and-how-does-it-work.

[3] See, for example, the website of Prudential Financial, Inc.: “we see strong opportunities in affordable housing equity.”

https://www.prudential.com/links/about/corporate-social-responsibility/impact-investing/active-capital/.

[4] Equity investors may seek projects with minimum numbers of units. See, e.g., the affordable housing Conventional Equity term sheet of Enterprise Community Investment, Inc., available at https://www.enterprisecommunity.org/sites/default/files/media-library/financing-and-development/conventional-equity/enterprise-conventional-equity.pdf .

[5] In a recent Annual Impact Investment Survey conducted by the Global Impact Investing Network, over 60% of investors reported that they track the financial performance of their investments alongside the Sustainable Development Goals (SDGs) set forward by the United Nations. See https://thegiin.org/assets/GIIN_AnnualImpactInvestorSurvey_2017_Web_Final.pdf (last accessed 2/21/19).

[6] See https://www.ft.com/content/85eeba58-746a-11e8-bab2-43bd4ae655dd.v

[2] While it is beyond the scope of this Toolkit, a tax credit program exists for developing businesses, something of a corollary to the LIHTC program for residential development: the New Markets Tax Credit Program. See www.cdfifund.gov/Documents/NMTC%20Target%20Areas%20QA.pdf and www.taxpolicycenter.org/briefing-book/what-new-markets-tax-credit-and-how-does-it-work.

[3] See, for example, the website of Prudential Financial, Inc.: “we see strong opportunities in affordable housing equity.”

https://www.prudential.com/links/about/corporate-social-responsibility/impact-investing/active-capital/.

[4] Equity investors may seek projects with minimum numbers of units. See, e.g., the affordable housing Conventional Equity term sheet of Enterprise Community Investment, Inc., available at https://www.enterprisecommunity.org/sites/default/files/media-library/financing-and-development/conventional-equity/enterprise-conventional-equity.pdf .

[5] In a recent Annual Impact Investment Survey conducted by the Global Impact Investing Network, over 60% of investors reported that they track the financial performance of their investments alongside the Sustainable Development Goals (SDGs) set forward by the United Nations. See https://thegiin.org/assets/GIIN_AnnualImpactInvestorSurvey_2017_Web_Final.pdf (last accessed 2/21/19).

[6] See https://www.ft.com/content/85eeba58-746a-11e8-bab2-43bd4ae655dd.v

i) Mission Equity Investing By Foundations

Foundations and other mission-based organizations may make mission-driven equity investments in addition to the grants and loans discussed above. Such equity investments seek a financial return in addition to a measurable social or environmental benefit, but the return sought may be “concessionary” (i.e. below-market rate), in support of the organization’s programmatic objectives.

ii) Impact Fund Equity Investing

Impact funds pool their investors’ contributions seeking to generate a measurable, beneficial social or environmental impact alongside a financial return. Bridges Ventures’ UrbanView fund, launched in 2017, is one example of a real estate impact fund (albeit focused on urban settings). http://www.bridgesfundmanagement.com/us/bridges-launches-urbanview-impact-driven-us-real-estate-vehicle/. Avanath Capital Management is a privately held, vertically integrated investment firm which acquires, owns, renovates, and operates affordable, workforce, and value-oriented apartment communities.

f) Potential Advantages for Developers and Investors Presented by Supportive Housing – and Perceived Disadvantages

Whether one is going to be making the case in favor of investing in supportive housing projects, or in favor of including supportive units in larger affordable housing, it is helpful to educate oneself about the advantages these may present, and to anticipate the risks as others may perceive them.

To start with, bear in mind that supportive housing is a subcategory of affordable housing. Affordable housing offers low relative risk and a variety of attractive characteristics. These include a huge potential market (more than 50% of U.S. households would income-qualify for affordable housing), dramatic, nation-wide shortage of supply, and high demand during strong economic cycles. Demand for affordable housing rises even further during weak economic cycles, counter-cyclical performance which might attract hedging investors. An affordable rental housing preservation private equity fund can be structured to provide current income and short duration, which facilitates earlier return of capital to investors relative to traditional private equity funds. For example, affordable housing preservation bridge funds exist offering five-year terms; compare to traditional ten-year private equity fund terms.

Including supportive housing units in an affordable housing project may have additional advantages to offer developers and their investors:

Supportive housing may also impose particular perceived risks to developers of affordable housing, their potential investors, or affordable housing funding agency staff:

While SSI or other sources may cover projected individual rents, the viability of a supportive housing setting is dependent upon funding of operations. Families and human services professionals grow accustomed to the narrow margins of operating in a Medicaid-funded system, in which shortfalls are covered each eleventh-hour through corner-cutting, fund-shifting, fund-raising, and prayer. Funders, however, such as banks and housing agencies, have market expectations and corresponding underwriting rules. They will require a pro forma operating budget in which not only are costs projected to be covered, but also that inflation is accounted for and reserves are maintained for the unexpected costs which inevitably arise (and to cover temporary shortfalls, for example arising due to tardy governmental payors). A prospective developer of affordable housing may find it challenging to create a supportive housing operating budget which convincingly meets such underwriting requirements

While Medicaid dollars never go directly to an individual’s rent, the viability of a supportive housing setting is typically dependent upon the continued flow of Medicaid dollars to fund operations, particularly staff. Thus a shift in state priorities or federal Medicaid policy can make an entire supportive setting nonviable overnight, even though the ability of each individual resident to afford to pay their rent has not changed. Recent examples in New Hampshire include a group home model for girls, which was de-funded, and a supported boarding-house model for persons with mental illness, which was de-funded. This risk does not mean that such a property will inevitably fall fallow (the boarding-house is now a recovery residence). But it is important to anticipate how a developer, investor or housing agency staff person may view your prospective housing setting and to think about ways to reduce the perception of public policy risk with respect to that setting.

To start with, bear in mind that supportive housing is a subcategory of affordable housing. Affordable housing offers low relative risk and a variety of attractive characteristics. These include a huge potential market (more than 50% of U.S. households would income-qualify for affordable housing), dramatic, nation-wide shortage of supply, and high demand during strong economic cycles. Demand for affordable housing rises even further during weak economic cycles, counter-cyclical performance which might attract hedging investors. An affordable rental housing preservation private equity fund can be structured to provide current income and short duration, which facilitates earlier return of capital to investors relative to traditional private equity funds. For example, affordable housing preservation bridge funds exist offering five-year terms; compare to traditional ten-year private equity fund terms.

Including supportive housing units in an affordable housing project may have additional advantages to offer developers and their investors:

- Supportive housing residents typically have sources of income, in particular SSI, which are more reliable than the employment-based income of other low-income tenants. This can reduce a developer’s risks of delinquency and non-payment.

- Returns on investment in market-rate housing are highly impacted by renter turn-over costs. Market-rate multifamily community turnover rates can be as high as 50%.[1] Turn-over of supportive housing tenancies is typically considerably less frequent than turn-over of other categories of renters. This can reduce a developer’s turn-over costs.

- Pre-occupancy tenant vetting of supportive housing units will typically be performed by the organizing providing supports in the units, which can also reduce a developer’s turn-over costs.

- Any occupancy rate under 100% will impact investor returns. Properly-managed supportive housing units will always have a waitlist, so that a unit which becomes vacant can be re-occupied by a paying tenant relatively quickly. This can reduce a developer’s vacancy costs.

- Supportive housing residents will typically be in the lowest-income tier, potentially creating an opportunity for a developer to be granted additional points in the scoring of their application for competitive funding opportunities, such as LIHTCs.

- State affordable housing agencies may have specialized funding available for special needs developments; including supportive housing units in a planned development may create an opportunity for a developer to access such special needs funding.

Supportive housing may also impose particular perceived risks to developers of affordable housing, their potential investors, or affordable housing funding agency staff:

- Supportive housing may be seen as imposing operating funding risk.

While SSI or other sources may cover projected individual rents, the viability of a supportive housing setting is dependent upon funding of operations. Families and human services professionals grow accustomed to the narrow margins of operating in a Medicaid-funded system, in which shortfalls are covered each eleventh-hour through corner-cutting, fund-shifting, fund-raising, and prayer. Funders, however, such as banks and housing agencies, have market expectations and corresponding underwriting rules. They will require a pro forma operating budget in which not only are costs projected to be covered, but also that inflation is accounted for and reserves are maintained for the unexpected costs which inevitably arise (and to cover temporary shortfalls, for example arising due to tardy governmental payors). A prospective developer of affordable housing may find it challenging to create a supportive housing operating budget which convincingly meets such underwriting requirements

- Supportive housing may be seen as imposing public policy risk.

While Medicaid dollars never go directly to an individual’s rent, the viability of a supportive housing setting is typically dependent upon the continued flow of Medicaid dollars to fund operations, particularly staff. Thus a shift in state priorities or federal Medicaid policy can make an entire supportive setting nonviable overnight, even though the ability of each individual resident to afford to pay their rent has not changed. Recent examples in New Hampshire include a group home model for girls, which was de-funded, and a supported boarding-house model for persons with mental illness, which was de-funded. This risk does not mean that such a property will inevitably fall fallow (the boarding-house is now a recovery residence). But it is important to anticipate how a developer, investor or housing agency staff person may view your prospective housing setting and to think about ways to reduce the perception of public policy risk with respect to that setting.

g) Local Banks

Borrowing to fund the purchase or construction of multi-family residential housing differs in significant ways from taking a mortgage on one’s own home. For multi-family residential, banks will typically only offer fixed rate lending with a term five to seven years, at most. I/DD Supported Housing projects, relying on fixed streams of government income, typically can’t accommodate fluctuating interest rates. Our projects need fifteen to twenty year terms (ideally thirty year terms, if that were realistic).

Don’t underestimate the value of establishing a personal relationship with the leader of a local bank. With such a relationship, you could consider arranging a visit to the bank’s corporate headquarters with the local branch leader to discuss with senior officers of the institution the possibility of crafting something combining a loan with some corporate giving from the bank. Most local banks have a desire and the incentive to be good citizens. Your project may represent an attractive one with which the bank might want to be associated.

While there are no relevant discounted loan products, a lender might make concessions on term or underwriting. Be aware that doing so would commit the lender to making a “specialty” loan, requiring them to keep the risk for the life of the loan (“held in portfolio”) rather than, as if normally done, selling some or all of the loan to an outside entity.

Don’t underestimate the value of establishing a personal relationship with the leader of a local bank. With such a relationship, you could consider arranging a visit to the bank’s corporate headquarters with the local branch leader to discuss with senior officers of the institution the possibility of crafting something combining a loan with some corporate giving from the bank. Most local banks have a desire and the incentive to be good citizens. Your project may represent an attractive one with which the bank might want to be associated.

While there are no relevant discounted loan products, a lender might make concessions on term or underwriting. Be aware that doing so would commit the lender to making a “specialty” loan, requiring them to keep the risk for the life of the loan (“held in portfolio”) rather than, as if normally done, selling some or all of the loan to an outside entity.

i) The Community Reinvestment Act

The Community Reinvestment Act[1] (“CRA”) is designed to encourage banks to lend into low- and moderate-income communities. It does not involve a subsidy or preferred rate, but seeks to incentivize banks by making the bank’s CRA compliance record an issue to be considered by regulatory agencies when the banks seek to acquire, merge, or open new branches. It can’t hurt to raise the issue with your local bank if you believe your project may qualify.

View Footnotes

[1] Public Law 95-128, 91 Stat. 1147, title VIII of the Housing and Community Development Act of 1977, 12 U.S.C. § 2901 et seq.

h) Opportunity Zones

The 2017 federal Tax Cuts and Jobs Act created Opportunity Zones, designed to drive investment in underserved areas, bring investors to otherwise overlooked investment opportunities, incentivize long-term equity investments, including in real property, and encourage economic growth and job creation in underserved communities. In particular, it has the potential to attract high net worth individual investors to community development finance. The details are complex,[1] but essentially the program offers relief on taxes on capital gains invested in Opportunity Zones and on any subsequent gain in the Opportunity Zone investment. There are no reporting requirements, state oversight, or investment mandates. New Hampshire’s zone designations (selected by the Governor) last for ten years.

View Footnotes

[1] For a detailed New Hampshire-centric discussion, see the PowerPoint Opportunity Zone Review for New Hampshire Communities (October 2, 2018), available at: https://www.nheconomy.com/getattachment/grow/Opportunity-Zones/OZ-presentation10-28.pdf?lang=en-US (last accessed 2/21/19).